Time: 2023-10-31

Time: 2023-10-31  Views: 705

Views: 705

[Foreword]

The reason why Decision is highly praised by enterprises during the implementation of digital transformation projects is because experts are escorting Decision during the project process to help enterprises gain new knowledge, grow new capabilities, and improve management during the implementation of digital transformation projects. To improve our vision and reduce project misunderstandings, we have specially set up a "Decision Expert Column" to share with you a series of articles on the implementation of digital transformation projects, so stay tuned.

This article is based on Mr. Yang Yongqing, Decision’s chief financial expert, who has 24 years of rich experience in the field of SAP ERP, and combines the common misunderstandings he found in the implementation of ERP projects to publish corresponding research insights and suggestions to protect your SAP financial implementation and delivery.

[Problem Description]

1. When analyzing online monthly statements, the CFO of a multinational group company questioned why the sales cost difference accounts in the report of our group's European subsidiaries were divided into: price difference, exchange rate difference, production difference (further subdivided into nine differences), outbound delivery Differences, supplier consignment differences, material conversion differences? Why does the sales cost difference of the mainland China subsidiary have only one account?

2. The FICO consultant who is in the process of online implementation asked, is it feasible to set the cost difference account as follows? This is also the setting recommended by senior consultants in the past. Can it continue to be used in the system?

[Problem analysis]

Problem analysis one:

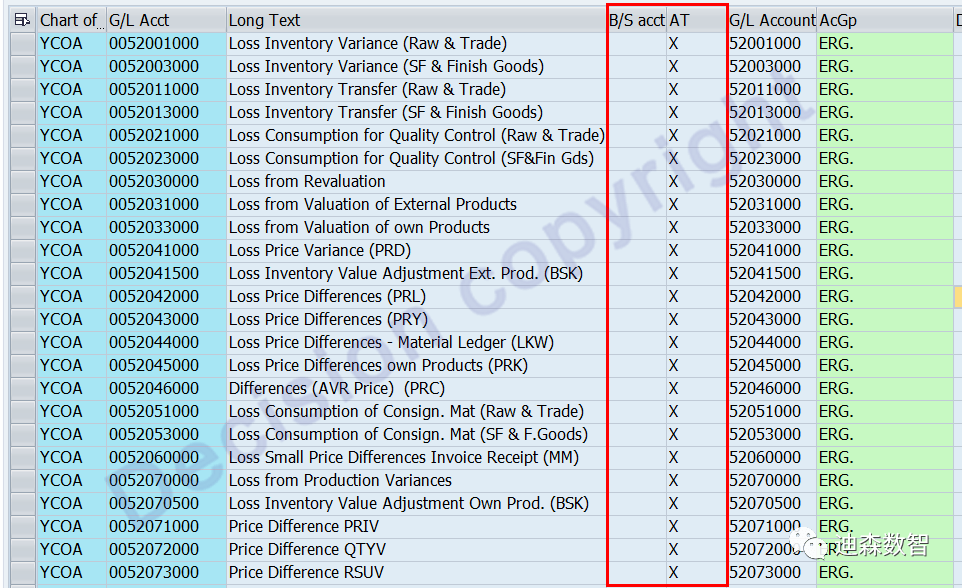

① Yes, the subject reference breakdown of SAP cost differences: price differences, exchange rate differences, production differences (further subdivided into nine differences), outbound differences, supplier consignment differences, material conversion differences, the following is the SAP IDES demonstration system Standard accounts in: Accounts starting with 0052* are all profit and loss accounts, non-asset and liability accounts.

② Western accounting cost accounting is based on standard cost assessment, and the cost difference is fully included in the profit and loss. Therefore, various differences that occur during the current period can be listed on the income statement (income statement).

③ China's accounting cost accounting is based on actual costs. Cost differences are temporarily listed as assets and liabilities inventory accounts, and are proportionally allocated to outbound and closing inventory at the end of the period. Therefore, various differences that occur on the cost difference debit side of the current period cannot be directly transferred to the profit and loss statement (income statement). They need to be summarized with the cost differences at the beginning of the period and then calculated and carried forward, and are based on the material movement of raw materials, semi-finished products, and finished products. Variances carried forward from the production process. The cost difference under the actual cost is the difference after aggregation and weighted calculation.

④ During actual cost accounting (material ledger operation), can the differences be carried forward in detail according to the types of occurrences mentioned above?

No, because:

4.1 The difference is relative. For example, the following is the standard input and output

ROH-1 raw material 3 pieces 3 yuan à production investment à HALB-1 semi-finished product 1 piece 3 yuan

HALB-1 semi-finished product 1 piece 3 yuan à production investment à FERT-1 finished product

If 1 ROH-1 (1 yuan each) is consumed in the production of semi-finished product HALB-1, then the cost difference of 1 yuan for HALB-1 is: input quantity variance (Input quantity variance). When the difference is rolled up to FERT, the cost price of HALB-1 changes from the standard 3 yuan to 4 yuan. When FERT produces finished products, the semi-finished product HBLB-1 is normally invested. The cost difference of 1 yuan for FERT-1 is: input price variance.

4.2 During actual cost accounting (material ledger operation), differences cannot be distinguished in detail. Currently, the SAP system only distinguishes: PRD (price difference), KDM (exchange rate difference). KDM exchange rate differences mainly calculate the exchange rate impact of foreign currency purchases, which are calculated and presented separately. All other differences are merged into PRD differences.

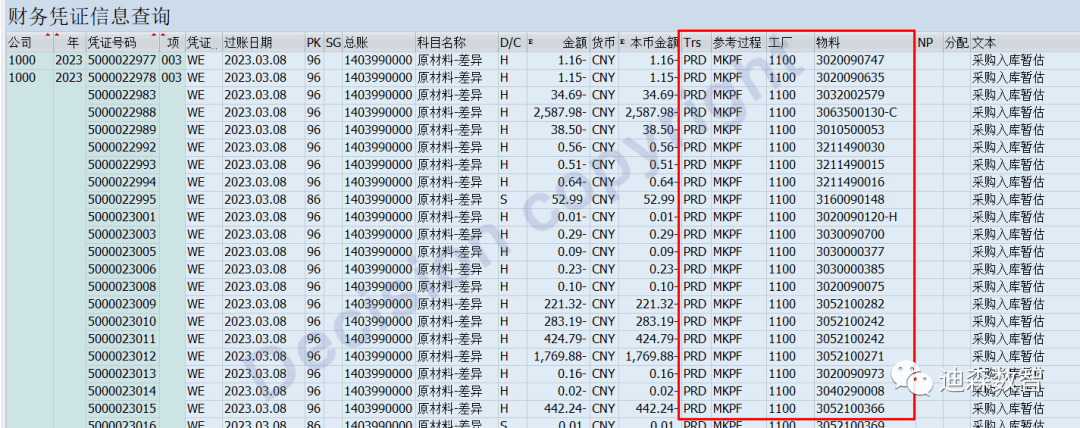

⑤ When doing actual cost accounting (material ledger operation), how can Chinese companies quickly query the various sources of cost differences like European and American companies? This problem is easy to handle. You can directly associate the ACDOCA table with the BKPF table to make a report. Simply assemble a QUERY report with the SQ01/SQ02/SQ03 transaction code. The cost difference amount query report (ZQFI201) we made is as follows:

After querying the occurrence amount of the cost difference account, you can classify the source of the lender's difference type by combining the following three fields.

ACDOCA-KTOSL Transactions/Transactions

BKPF-BLART Voucher Type

BKPF-AWTYP reference transaction, the main classification description is as follows:

BKPF FI manual voucher

MLHD Material Ledger Voucher

PRCHG material price adjustment, material inventory amount adjustment

MKPF material inbound or outbound

RMRP Purchase Settlement Difference

AUAK production order settlement

Problem analysis two:

① Such cost difference accounts are not suitable for Chinese companies, because Chinese companies need to calculate actual costs (material ledger operation).

② In actual projects, financial personnel often have to explain the sources and whereabouts of cost differences to internal and external personnel. The trouble is that the actual cost of SAP (material ledger operation) always has cost differences that cannot be eliminated. Coupled with the manual adjustment processing by financial personnel, it is difficult to explain the ins and outs of the differences.

③ In actual projects, financial personnel often have to explain the sources and whereabouts of cost differences to internal and external personnel. The trouble is that the actual cost of SAP (material ledger operation) always has cost differences that cannot be eliminated. Coupled with the manual adjustment processing by financial personnel, it is difficult to explain the ins and outs of the differences.

④ For the S4 HANA system, single-layer cost difference PRY and multi-layer cost difference PRV are no longer distinguished, and are unified into PRY, that is, PRV is no longer used and distinguished. So the account "1404090200ML multi-level difference carry forward" is redundant.

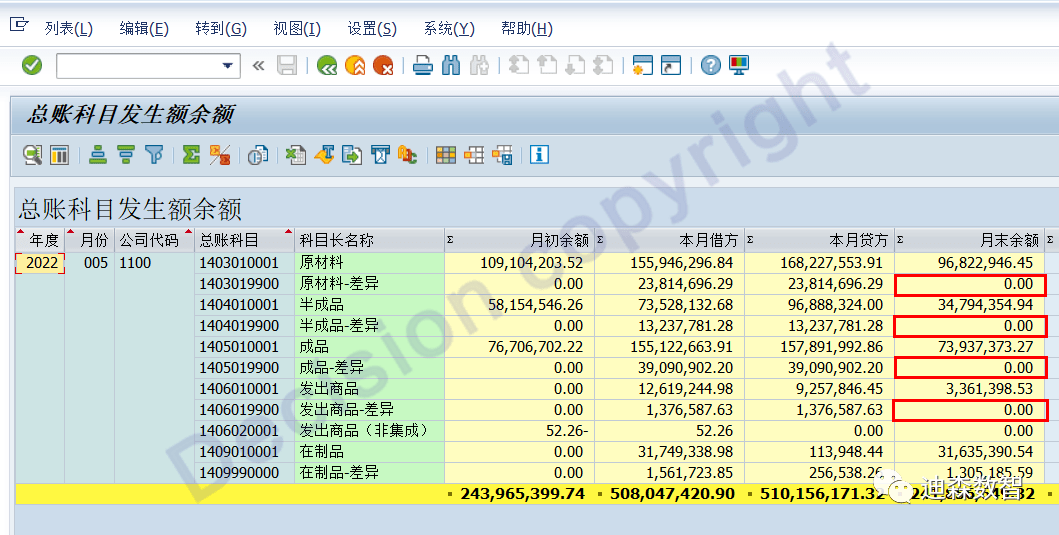

⑤ In the actual project, the total cost difference account setting is: set up a cost difference account for raw materials, semi-finished products, inventory goods, and shipped goods respectively (as shown below). After the actual cost at the end of the period (material ledger operation) is settled, you only need to view Whether these difference accounts are 0, you will know whether the differences have been processed.

If the balance of a certain cost difference account is not 0, you can query the report (ZQFI201), summarize by account + factory + material + period, and you can immediately query which factory and material have the difference.

【Service Guide】

For more information on SAP courses, project consultation and operation and maintenance, please call Decision's official consultation hotline: 400-600-8756

【About Decision】

Global professional consulting, technology and training service provider, SAP gold partner, SAP software partner, SAP implementation partner, SAP official authorized training center. Seventeen years of quality, trustworthy!